Trading Strategies Python: Develop, Backtest & Automate

Land Your First Data Science Job

A proven roadmap to prepare for $75K+ entry-level data roles. Perfect for Data Scientist ready to level up their career.

TL;DR

- Python is a powerful tool for trading due to its simplicity, flexibility, and robust libraries ideal for implementing diverse trading strategies, from manual to algorithmic.

- Key Python libraries like Pandas, NumPy, and Backtrader enable traders to analyze data and backtest strategies effectively, improving decision-making and strategy validation.

- Implementing sound risk management practices, such as diversification and stop-loss mechanisms, is crucial for minimizing risks and optimizing returns in Python-based trading strategies.

- With its increasing role in algorithmic trading, Python remains essential for developing and automating strategies, ensuring they adapt to evolving market conditions.

Introduction

Python has rapidly become one of the most popular programming languages among traders and financial analysts, thanks to its simplicity, readability, and extensive libraries tailored specifically for trading. Its versatility allows traders of all skill levels to implement strategies ranging from simple, manual methods to complex algorithmic approaches.

This guide covers a comprehensive range of topics related to trading strategies in Python. We will explore foundational concepts and gradually move to advanced, algorithm-driven strategies. The content is structured to provide clarity for beginners while offering depth and actionable insights for experienced traders.

Traders benefit significantly by utilizing Python, primarily through automation, flexibility, and robust backtesting capabilities. Automation reduces manual errors and saves valuable time, while Python's flexibility allows traders to quickly adapt and refine strategies according to market conditions. Additionally, powerful backtesting tools help traders thoroughly test and validate their strategies against historical data before risking real capital.

Why Python for Trading?

Python has emerged as one of the leading programming languages for developing and implementing trading strategies, primarily due to several inherent advantages it holds over alternative languages. Firstly, Python is open-source, meaning it is freely accessible, customizable, and supported by a vast community of developers worldwide. This extensive community facilitates rapid knowledge sharing, troubleshooting, and continuous improvements. Moreover, Python's strength lies in its extensive libraries specifically tailored for data analysis, algorithmic trading, and financial modeling. Popular libraries like Pandas, NumPy, and Scikit-learn offer powerful tools for market analysis, data manipulation, and machine learning, making Python an ideal choice for traders.

Real-world use cases further reinforce Python's dominance in trading. Both retail traders and institutional investors utilize Python for various purposes, including algorithmic strategy development, high-frequency trading, risk management, and quantitative research. Python's flexibility and readability allow traders to quickly prototype, test, and deploy complex trading algorithms.

According to Investopedia, algorithmic trading has grown significantly over the past decades, and Python has played a central role in this development due to its ease of use, robust libraries, and suitability for handling large datasets efficiently (Investopedia: Algorithmic trading's growth and Python's role). As algorithmic trading continues to expand, Python's importance as a foundational tool for traders and financial institutions is likely to grow further.

Fundamental Trading Concepts

Overview of Trading Strategies

Trading strategies can broadly be categorized into two approaches: manual and algorithmic. Manual trading involves a human trader making buying and selling decisions based on market analysis, intuition, or experience. Algorithmic trading, on the other hand, leverages pre-programmed rules executed automatically by computers, providing speed, precision, and consistency.

Traders also distinguish between discretionary and systematic methods. Discretionary trading relies heavily on the trader's judgment and market interpretation, allowing flexibility but also introducing emotional biases. Systematic trading eliminates emotional decision-making by following clearly defined, repeatable rules and criteria.

Risk Management Basics

Effective risk management is critical for long-term trading success. Two fundamental techniques include stop-loss orders and position sizing. A stop-loss order helps automatically limit potential losses by closing a position once a predefined level is reached. Position sizing involves determining the appropriate amount of capital to allocate to each trade, balancing the potential returns against acceptable risk.

Core Market Data Types

Trading strategies depend on different types of market data, primarily prices, volumes, and indicators. Price data provide essential information about market movements and trends. Volume data reveal the quantity of assets traded over a period, which traders often use to confirm the strength or weakness of price movements. Technical indicators, such as moving averages, RSI (Relative Strength Index), and MACD (Moving Average Convergence Divergence), offer deeper insights into market conditions, helping traders identify potential entry and exit points.

Setting Up Your Python Trading Environment

To effectively develop trading strategies in Python, you must first set up an appropriate Python environment. Begin by installing Python from the official website, ensuring you choose the latest stable version. Alongside Python, it's essential to install tools such as pip, Python's package installer, which simplifies library management.

For writing, testing, and debugging code, select an integrated development environment (IDE) tailored to your workflow. Popular IDEs among algorithmic traders include Jupyter Notebook, Visual Studio Code (VS Code), and PyCharm. Jupyter Notebook is widely favored for interactive analysis and experimentation, while VS Code and PyCharm offer robust coding environments suitable for larger projects. For detailed, step-by-step guidance on setting up your environment, refer to QuantInsti's setup instructions.

Key Python Libraries for Trading

Several Python libraries form the backbone of algorithmic and quantitative trading strategies:

- NumPy and Pandas: These foundational libraries are critical for numerical operations and data manipulation. NumPy efficiently handles arrays and mathematical functions, while Pandas simplifies data analysis tasks, especially for handling financial time-series data.

- TA-Lib: Widely adopted for technical analysis, TA-Lib provides a broad range of indicators such as moving averages, RSI, MACD, and Bollinger Bands, streamlining the process of developing trading signals.

- Backtrader and Zipline: Essential for backtesting strategies, these libraries allow traders to simulate their algorithms on historical data, evaluate performance metrics, and optimize trading parameters.

- Data Access Libraries (yfinance, Alpha Vantage APIs): Reliable and easy-to-use data sources are vital. Libraries like

yfinanceand APIs such as Alpha Vantage provide straightforward methods to download historical and real-time market data, helping traders efficiently gather necessary information.

For a comprehensive overview of these libraries and their respective roles in trading strategy development, see the detailed explanation provided by Towards Data Science.

Core Trading Strategies Implemented in Python

1. Buy and Hold

Buy and hold is one of the simplest trading strategies, involving purchasing assets with the intention of holding them for a long period, regardless of short-term market fluctuations. It works best in steadily rising markets, benefiting from long-term upward trends and minimizing transaction costs. However, it performs poorly during prolonged bearish market periods and doesn't capitalize on short-term opportunities.

Example implementation in Python:

import yfinance as yf

# Download historical data for Apple stock

data = yf.download('AAPL', start='2010-01-01', end='2023-01-01')

# Calculate returns assuming buy and hold

initial_price = data['Close'][0]

final_price = data['Close'][-1]

returns = (final_price - initial_price) / initial_price

print(f"Buy and hold returns: {returns * 100:.2f}%")

2. Moving Averages (SMA, EMA)

Moving averages are technical indicators used to detect market trends, smooth price data, and generate trading signals. The Simple Moving Average (SMA) gives equal weight to all data points, whereas the Exponential Moving Average (EMA) emphasizes recent price action.

Python code snippet for SMA and EMA crossover signal generation:

import pandas as pd

import numpy as np

# Calculate SMA and EMA

short_window = 50

long_window = 200

data['SMA_short'] = data['Close'].rolling(window=short_window).mean()

data['EMA_long'] = data['Close'].ewm(span=long_window, adjust=False).mean()

# Generate signals

data['Signal'] = np.where(data['SMA_short'] > data['EMA_long'], 1, 0)

data['Position'] = data['Signal'].diff()

3. Momentum Strategies

Momentum strategies rely on the assumption that assets performing well recently will continue to perform well in the near future. These strategies typically involve buying recent winners and selling recent losers. While momentum strategies can outperform during trending markets, they can experience sharp reversals and large drawdowns.

A detailed sample Python implementation can provide further practical insights into the logic and performance of momentum trading.

4. Mean Reversion

Mean reversion strategies are based on the theory that asset prices tend to revert to their historical mean or average over time. Traders identify assets deviating significantly from historical averages, anticipating a reversal. While theoretically straightforward, mean reversion strategies require careful parameter tuning and risk management to avoid persistent trends.

Example Python code for mean reversion:

# Calculate z-score for mean reversion strategy

data['rolling_mean'] = data['Close'].rolling(window=20).mean()

data['rolling_std'] = data['Close'].rolling(window=20).std()

data['z_score'] = (data['Close'] - data['rolling_mean']) / data['rolling_std']

# Generate buy/sell signals based on z-score threshold

entry_threshold = -2

exit_threshold = 0

data['Long'] = np.where(data['z_score'] < entry_threshold, 1, 0)

data['Exit'] = np.where(data['z_score'] > exit_threshold, 1, 0)

5. Advanced Strategies

Advanced strategies use sophisticated approaches like machine learning (ML) to analyze market patterns. Supervised learning methods, such as regression and classification, predict future prices or trading signals. Unsupervised learning techniques, such as clustering, identify hidden patterns or anomalies. Algorithmic execution automates trade placements based on model predictions, enhancing consistency and efficiency.

For a comprehensive look at integrating ML and automation in Python-based trading, see QuantInsti's guide.

Data Acquisition and Processing

Effective trading strategies built with Python require reliable financial data. Common sources of financial data include platforms such as Yahoo Finance, Quandl, and APIs provided by brokers. Yahoo Finance is popular for its accessibility and free historical data, making it suitable for initial strategy testing. Quandl provides extensive datasets, both free and premium, covering various asset classes and economic indicators. Broker APIs, offered by platforms like Interactive Brokers or Alpaca, deliver real-time market data and facilitate seamless integration with trading execution systems.

Financial data obtained from these sources typically comes in various formats, including CSV files, JSON responses, and live API feeds. CSV files provide simple tabular data that can be easily loaded into tools such as Pandas for analysis. JSON is widely used for API responses and can be efficiently parsed within Python scripts. Live API feeds provide real-time data streams, enabling strategies to respond instantly to market changes.

Before performing any analysis, raw data typically requires cleaning and preparation. Common preprocessing tasks include handling missing data, adjusting or normalizing prices, and aligning different datasets by timestamps. Python libraries such as Pandas and NumPy are widely used to streamline these steps. Properly cleaned and formatted data ensure accuracy and efficiency in strategy modeling and backtesting.

Backtesting and Evaluating Strategies

Importance of Historical Testing

Backtesting is a critical component of developing effective trading strategies. By evaluating how a strategy would have performed using historical market data, traders can gain valuable insights into its potential profitability, robustness, and reliability. Historical testing helps identify strengths and weaknesses in a strategy before committing real capital and can highlight flaws that might not be obvious when simply analyzing theoretical performance.

Using Backtrader/Zipline for Backtesting

Python-based frameworks like Backtrader and Zipline offer robust tools for strategy backtesting. Backtrader is known for its simplicity, flexibility, and detailed documentation, making it suitable for beginners and advanced traders alike. Zipline, developed by Quantopian, provides extensive data handling capabilities and seamless integration with pandas, catering to users who require advanced analytics and data processing.

These libraries allow traders to simulate strategy performance over historical data, providing insights into potential profitability, trade frequency, and risk exposure.

Walkthrough: Backtest a Sample Strategy

Below is a simplified example of how you might backtest a basic moving average crossover strategy using Backtrader:

import backtrader as bt

class MovingAverageCrossStrategy(bt.Strategy):

def __init__(self):

self.fast_ma = bt.indicators.SimpleMovingAverage(self.data.close, period=10)

self.slow_ma = bt.indicators.SimpleMovingAverage(self.data.close, period=30)

def next(self):

if not self.position:

if self.fast_ma[0] > self.slow_ma[0]:

self.buy()

elif self.fast_ma[0] < self.slow_ma[0]:

self.sell()

cerebro = bt.Cerebro()

cerebro.addstrategy(MovingAverageCrossStrategy)

data = bt.feeds.YahooFinanceData(dataname='AAPL', fromdate='2020-01-01', todate='2022-12-31')

cerebro.adddata(data)

cerebro.run()

cerebro.plot()

This code snippet initializes a simple moving average crossover strategy, backtests it over two years of Apple stock data, and plots the results.

Risk Metrics: Sharpe Ratio, Drawdown, Win Rate

Evaluating strategy performance also involves analyzing risk-adjusted metrics:

- Sharpe Ratio: Measures excess return per unit of volatility, indicating how well the returns compensate for the risk taken.

- Drawdown: Represents the largest peak-to-trough decline in portfolio value, highlighting the maximum potential loss.

- Win Rate: Indicates the percentage of profitable trades, providing insight into the strategy's consistency.

Incorporating these metrics into your analysis helps ensure that your strategy is not only profitable but also aligned with your risk tolerance and trading objectives.

Building and Automating a Trading Bot

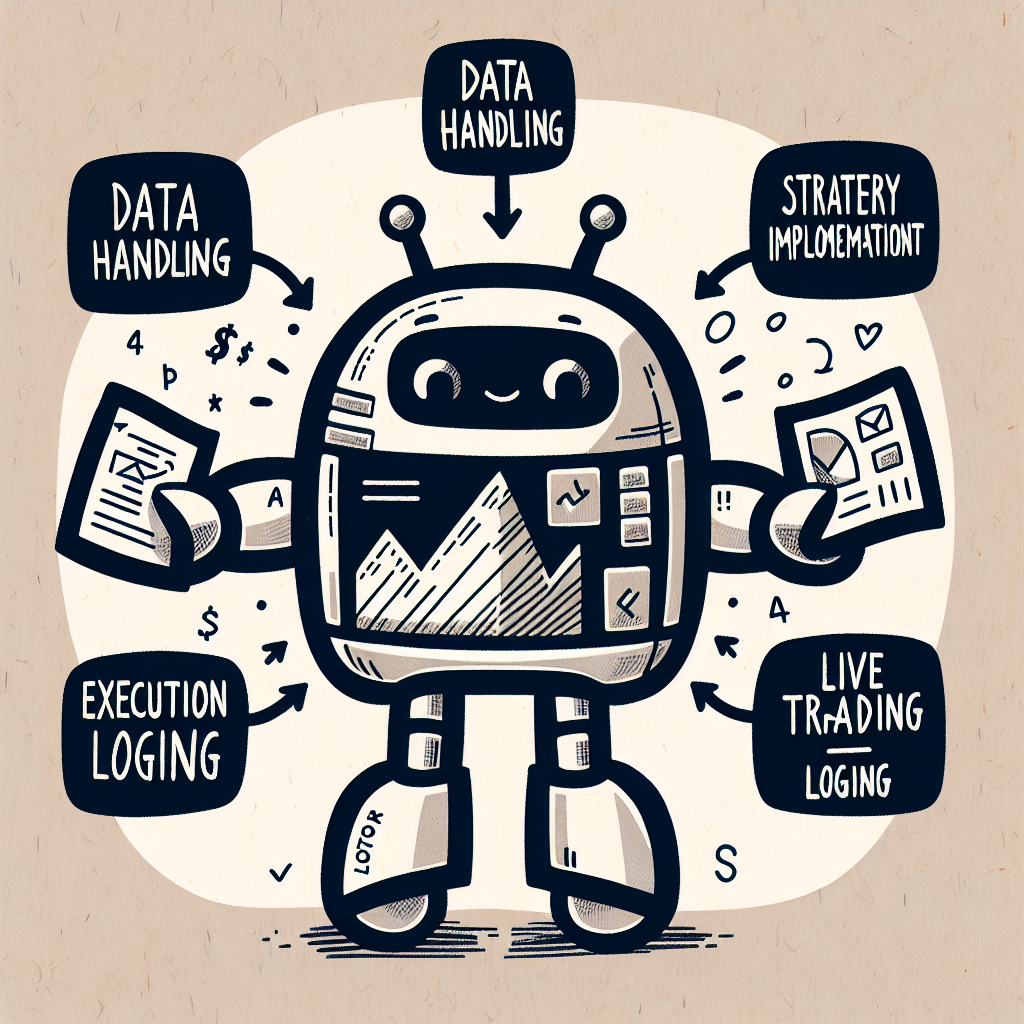

Designing a Robust Bot Architecture

A well-designed trading bot for algorithmic trading should have a modular architecture, making it easier to develop, test, and maintain. Typically, this modular structure includes distinct sections dedicated to data handling, strategy implementation, execution, and logging.

- Data Module: Handles market data acquisition and preprocessing, ensuring accurate and timely data feeds for decision-making.

- Strategy Module: Encapsulates trading logic and signal generation. This module analyzes market data to generate buy, sell, or hold signals based on predetermined rules.

- Execution Module: Responsible for order placement, order tracking, and trade management. It interfaces directly with brokerage platforms to execute trades.

- Logging Module: Records critical information such as transaction histories, system performance, errors, and debugging information, providing transparency and ease of troubleshooting.

The key components of a robust trading bot architecture thus include data collection processes, the signal generation engine, and order management routines. Clear separations between these components enhance reliability, simplify debugging, and streamline future updates or modifications.

Deploying Your Trading System

Once your bot architecture is established, the next step is deployment. Traders typically choose between paper trading and live trading environments.

- Paper Trading: Allows testing of your bot in realistic market conditions without risking actual capital. It helps to validate trading strategies and catch potential issues early.

- Live Trading: Involves deploying the bot with real funds, requiring rigorous testing beforehand and careful monitoring during operation.

Integration with brokerage APIs is a critical part of deployment. Popular broker APIs such as Interactive Brokers and Alpaca offer extensive documentation and community support, simplifying the integration process. These APIs enable automated order placement, real-time data streaming, and account management functionalities.

Finally, monitoring and maintaining your trading bot is essential. Regularly reviewing the bot's performance, logs, and error reports enables early detection of issues. Scheduled maintenance ensures that the bot stays aligned with current market conditions, broker API updates, and changes within your trading strategy.

Risk Management and Best Practices

Effective risk management is essential for any trading strategy developed using Python. Incorporating robust risk management principles helps traders limit potential losses and optimize returns.

Setting Stop-Loss and Take-Profit Levels

Clearly defined stop-loss and take-profit levels are fundamental for risk control. Stop-loss orders automatically close out positions at predetermined loss limits, helping traders avoid significant drawdowns. Similarly, take-profit orders secure gains by closing trades when they reach target profit levels. Python-based algorithms can dynamically set these limits based on market volatility, historical data, or statistical models, enhancing flexibility and responsiveness.

Diversification and Capital Allocation

Diversification across multiple assets and strategies reduces the overall portfolio risk. Utilizing Python, traders can quantitatively assess correlations among securities, optimizing portfolio allocation and minimizing exposure to single-asset volatility. Allocating capital prudently among different strategies and asset classes ensures better stability and sustainable profitability over time.

Avoiding Overfitting in Backtests

Overfitting occurs when trading strategies perform exceptionally well in historical simulations but fail under live market conditions. To mitigate this risk, it's critical to employ best practices when backtesting strategies in Python. These include splitting historical data into training and testing periods, performing cross-validation, and keeping model parameters simple. Additionally, validating strategies across multiple market environments helps ensure robustness and generalizability.

Compliance and Ethical Considerations

Trading strategies developed in Python must adhere to regulatory compliance and ethical standards. Traders should ensure their algorithms comply with applicable financial regulations, including market manipulation prohibitions and data privacy laws. Additionally, maintaining transparent, fair, and ethical trading practices helps protect market integrity and promotes trust among market participants.

Troubleshooting and Optimization

When implementing trading strategies in Python, several common pitfalls can impact performance and reliability. Recognizing and managing these issues early can significantly improve strategy outcomes.

Common Pitfalls

- Data Errors: Incorrect, incomplete, or corrupted data can lead to inaccurate backtesting results and poor trading decisions. To avoid this, always verify data integrity, handle missing values carefully, and cross-reference data sources regularly.

- Slippage: The difference between the expected and actual execution price, known as slippage, can negatively affect strategy performance. To mitigate slippage, model realistic transaction costs in backtests and use conservative assumptions in simulations.

- Latency: Delays in data processing, order submission, or execution can lead to missed opportunities or suboptimal trades. Optimize your Python code and infrastructure to minimize latency, particularly if employing high-frequency trading strategies.

How to Tune and Improve Strategies

- Parameter Optimization: Systematically test different parameter values using techniques like grid search or randomized search to find optimal settings that maximize performance metrics.

- Robustness Testing: Evaluate your strategy performance across various market conditions and historical scenarios to ensure consistency and reduce susceptibility to overfitting.

- Performance Monitoring: Continuously track strategy metrics such as sharpe ratio, drawdown, and win rate. Regularly reviewing these metrics can help identify deteriorations early, prompting timely adjustments.

- Code Efficiency: Regularly optimize and refactor Python code to improve execution speed and reduce latency. Libraries such as NumPy, Pandas, and Cython can help achieve significant performance gains.

By proactively troubleshooting common issues and regularly tuning your strategies, you can enhance reliability and profitability in algorithmic trading.

Resources and Next Steps

To deepen your knowledge of trading strategies using Python, explore the following resources:

Recommended Books, Courses, and Communities

- Books:

- Python for Finance by Yves Hilpisch: Covers essential Python techniques specific to finance and algorithmic trading.

- Algorithmic Trading and DMA by Barry Johnson: Provides in-depth insights into algorithmic trading methods and market microstructure.

- Courses:

- Coursera's "Trading Algorithms" by Indian School of Business: Offers practical lessons on developing and backtesting trading strategies.

- Udemy's "Python for Financial Analysis and Algorithmic Trading": Features hands-on tutorials for beginners and intermediate traders.

- Communities:

- QuantConnect Community Forum: A vibrant platform for discussing and sharing algorithmic trading strategies developed in Python.

- Reddit's r/algotrading: Active community discussing resources, strategies, and projects related to algorithmic trading.

Further Reading

- Comprehensive guides and tutorials from QuantInsti: This resource provides extensive step-by-step tutorials and guides on developing and deploying trading strategies with Python.

Open-source Repositories and Sample Projects

- Zipline: A popular Python library for backtesting trading strategies. It provides a robust framework and extensive documentation.

- Freqtrade: An open-source crypto-currency trading bot written in Python, suitable for learning automated trading implementation.

- Awesome Quant GitHub Repository: Curated list of libraries, tools, and resources for quantitative finance and algorithmic trading in Python.

Conclusion

Python's versatility makes it a powerful tool for developing and implementing trading strategies. Its extensive libraries and frameworks allow traders to efficiently backtest, optimize, and automate their strategies, helping them remain competitive in the dynamic financial markets.

When beginning with Python-based trading strategies, it's beneficial to start small. Focus first on foundational concepts, gradually iterating and refining your approaches through rigorous backtesting. Backtesting not only validates your strategies but also provides valuable insights into their effectiveness under historical market conditions.

Finally, continuous improvement is essential in trading strategy development. Markets evolve, and strategies that work today may require adjustments tomorrow. Regularly researching new methodologies, staying current with market trends, and consistently updating your technical skill set will ensure your Python-based trading strategies remain robust and effective over time.

Land Your First Data Science Job

A proven roadmap to prepare for $75K+ entry-level data roles. Perfect for Data Scientist ready to level up their career.

Related Articles

Continue your learning journey with these related topics

Master Data Science in Days, Not Months 🚀

Skip the theoretical rabbit holes. Get practical data science skills delivered in bite-sized lessons – Approach used by real data scientist. Not bookworms. 📚